If you own more than one company (or plan to own), a Cyprus holding company is one of the most tax-efficient ways to consolidate them. Not only in Europe, but worldwide.

Zero tax on dividends flowing up from subsidiaries. Zero capital gains tax on the sale of a company. No withholding tax when distributing profits to shareholders. And if, as a Cyprus resident, you fall under the Non-Dom regime, the dividends you receive personally are also tax-free, except for a nominal GHS contribution of up to €4,770 per year.

This guide covers the full tax benefits of a Cyprus holding company: what it is, how the structure works, who it is suitable for, how it compares to other European holding locations, and what it saves you in practice.

Want to get started immediately? Check out our Cyprus holding company formation service →

What is a Cyprus holding company?

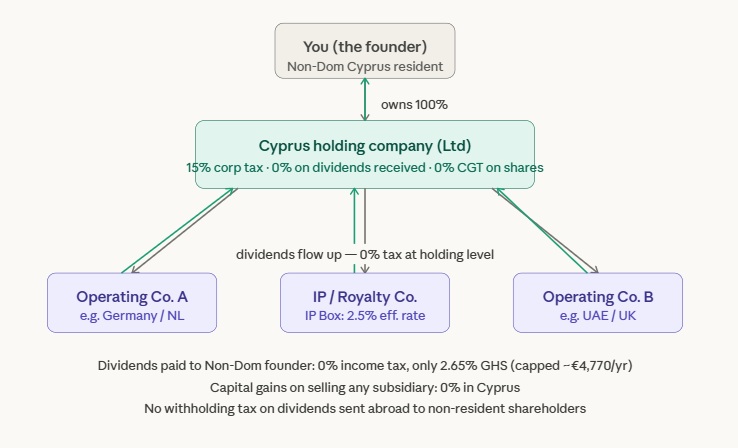

A Cyprus holding company is a private limited liability company (Ltd) whose primary purpose is to hold shares in other companies, subsidiaries, joint ventures, investment vehicles, or a combination thereof. It does not carry out day-to-day operational activities. It owns, consolidates, and controls.

The structure is simple: you are at the top as a shareholder, the Cyprus holding company is below you, and your operating companies are below the holding company. Profits flow upwards as dividends. When you eventually sell one of those companies, the capital gain falls into the holding company — and is taxed at 0%.

The holding company itself is incorporated under Cypriot Companies Law (Chapter 113), based on English Common Law. This is a significant detail for international investors: Cypriot contract structures, shareholder agreements, and corporate governance frameworks operate within a legal tradition that most Western and Middle Eastern entrepreneurs are already familiar with.

The tax benefits of a Cyprus holding company: the concrete figures

This is where Cyprus distinguishes itself. The combination of available exemptions is truly exceptional, even by EU standards.

15% corporate tax

Cyprus levies a corporate tax of 15% on net profit, placing it among the lowest rates in the European Union. For a holding company that primarily receives exempt dividends and holds shares, the effective rate on most income is well below that, often close to zero.

0% tax on dividends received from subsidiaries

This is the core benefit. Dividends received by a Cyprus holding company from its subsidiaries (both within and outside the EU) are fully exempt from both corporate income tax and Special Defence Contribution (SDC), provided that two conditions are met:

- The subsidiary derives no more than 50% of its activities from investment income

- The foreign tax burden on the subsidiary is not “substantially lower” than the Cypriot rate (the threshold is approximately 6.25%)

In practice, this exemption applies to the vast majority of operating companies. Your Dutch BV, your Belgian BVBA, your UK Ltd, your UAE LLC—dividends from all these entities flow completely tax-free to the Cyprus holding company.

For EU subsidiaries, the EU Parent-Subsidiary Directive further strengthens this by completely eliminating withholding tax at source on qualifying intra-EU dividend flows.

0% capital gains tax on share sales

Cyprus does not levy capital gains tax on the disposal of shares, bonds, or other securities. The only exception: if the relevant subsidiary owns real estate in Cyprus, the real estate portion falls outside the exemption.

What this means in practice: if you build a company in a subsidiary, grow it to €5 million, and sell it, the entire capital gain falls within the Cyprus holding company and is taxed at zero. You then distribute it to yourself as a dividend, also at zero if you are a Cypriot Non-Dominion resident.

0% withholding tax on outgoing dividends

Cyprus does not levy withholding tax on dividends paid by a Cypriot company to non-resident shareholders, regardless of their country of residence. This also makes Cyprus attractive for founders who do not personally reside in Cyprus. Your Austrian investor, your Dutch co-shareholder, your family office based in the UAE—none of them face a Cypriot withholding tax on distributions.

Compare this with the Netherlands (0–15%), Luxembourg (0–15%) and Ireland (0–25% depending on place of residence), … The Cypriot position is superior in this respect.

0% withholding tax on interest and royalties paid to non-residents

Cyprus also does not levy withholding tax on interest or royalty payments to non-resident companies or individuals. This is relevant for holding companies that lend money to subsidiaries (intra-group financing) or license IP to subsidiaries, both common strategies in international group structures.

65+ double taxation treaties

Cyprus has a network of double taxation treaties with more than 65 jurisdictions, including Germany, the Netherlands, the UK, India, Russia, the UAE, and most of Eastern Europe. These treaties reduce or eliminate withholding tax on income flowing from treaty countries to Cyprus, thereby further protecting the fiscal efficiency of the structure.

How Cyprus compares to other European holding companies

| Feature | Cyprus | The Netherlands | Luxembourg | Malta | Ireland |

|---|---|---|---|---|---|

| Corporate tax | 15% | 25,8% | 24,94% | ~5% (repayment system) | 15% |

| Dividend exemption | Yes | Yes (participation) | Yes (participation) | Yes (refund) | Partially |

| Capital gains tax on shares | 0% | 0% | 0% | 0% | 20% |

| Withholding tax on outgoing dividends | 0% | 0–15% | 0–15% | 0% | 0–25% |

| Withholding tax on interest/royalties | 0% | 0% | 0% | 0% | 20% |

| English Common Law | Yes | No | No | No | Yes |

| EU member | Yes | Yes | Yes | Yes | Yes |

| Typical start-up costs | ~€1.650 | €3.000–5.000+ | €5.000–10.000+ | €3.000–5.000+ | €3.000–5.000+ |

Cyprus does not win on treaty scope; the Netherlands and Luxembourg have broader networks. However, on the combination of a low corporate tax rate, 0% withholding tax on all outgoing payments, English Common Law, and incorporation costs, Cyprus surpasses every other EU jurisdiction for the typical holding structure on an enterprise scale.

Malta uses a repayment mechanism that achieves a comparable effective rate of ~5%, but is operationally more complex and less transparent for distribution purposes. The Netherlands and Luxembourg are excellent for large multinational structures, but significantly more expensive to manage with much higher substance requirements.

The Cyprus Holding + Non-Dom combination: the complete picture

For founders who move to Cyprus in person, tax efficiency goes even deeper.

Cyprus's Non-Dom regime exempts new residents from tax on dividend income and passive income for up to 17 years. The only costs are a 2.65% contribution to the National Health System (GHS), capped at approximately €4,770 per year, regardless of the size of the dividend.

Stack the holding company on top of Non-Dom and this is the end-to-end flow:

- Operating company earns €1,000,000 profit

- Subsidiary pays local corporate income tax (standard rate in home country)

- Subsidiary pays dividend to Cyprus holding company → 0% tax at holding level

- Holding company pays dividends to you personally → 0% income tax as a Non-Domaine

- You pay a maximum of €4,770 GHS per year, regardless of the size of the dividend.

Compare this with Belgium (30% withholding tax on dividends) or the Netherlands (26.9% substantial interest tax), and the annual savings for a high-earning entrepreneur quickly exceed €150,000 – €200,000 per year.

Adding the IP Box regime: effectively 2.5% on intellectual property income

If your company involves intellectual property: software, patents, algorithms, trademarks, or other qualifying intangible assets, the Cyprus IP Box regime a third layer of efficiency.

Income derived from qualifying IP held in a Cypriot company (including a holding company or a special IP subsidiary) is subject to an effective corporate tax rate of only 3%, achieved through an 80% deduction on qualifying IP profits.

A commonly used structure for IP-intensive companies: the Cyprus holding company owns the IP and grants licenses to operating companies worldwide. Royalties flow to Cyprus, taxed at 3%. The remaining profit is subsequently distributed as a dividend to the Non-Dom founder, at 0%.

For whom is a Cyprus holding company suitable?

A Cyprus holding structure makes the most financial sense when one or more of the following situations apply:

- You own or are building multiple companies. A holding company exists to consolidate. If you have one operating company, the benefits are real but modest. With two, three, or more, or if you plan to, the structure creates a clean, tax-efficient way to centralize ownership, distribute profits, and position yourself for a potential exit.

- You plan to sell a company within the next 5–10 years. The 0% capital gains tax on share sales is potentially the most valuable benefit of the structure. An exit of €5 million generates a tax bill of €1 million in most European jurisdictions. In Cyprus: zero.

- You receive dividends from foreign subsidiaries. If you currently route dividends from a Belgian or Dutch operating BV directly to yourself as a private individual, you lose 27–30% of that income to tax. A Cyprus holding structure eliminates withholding tax (via the Parent-Subsidiary Directive) as well as personal income tax (via Non-Domain).

- You are considering moving. If you are open to living in Cyprus, or already spend a lot of time here, the Non-Dom + holding combination is the most powerful legitimate tax structure available to European entrepreneurs. Cyprus has a strong Dutch-speaking expat community, an excellent climate, and a quality of life that makes the decision to move much simpler than it sounds on paper.

- You have IP or software assets. The IP Box + holding structure at a 3% effective rate is hardly replicable in other EU jurisdictions at comparable cost and simplicity.

Group exemption and loss set-off

An often overlooked benefit: if the holding company owns at least 75% of a subsidiary established in Cyprus, losses of one company in the group can be offset against profits of another in the same tax year.

This is particularly useful during the growth phase, when one operating company may be loss-making while another is profitable. Instead of passively deferring losses, you use them immediately.

Substance: what you need to have in order

Cyprus holding companies fully comply with OECD BEPS requirements and EU anti-abuse rules, but the structure delivers its benefits only if genuine substance is present. Substance means that the company is actually managed and controlled from Cyprus.

For most founder-led holding structures, substance is easy to build:

- At least one director residing in Cyprus with effective decision-making authority

- A registered office address in Cyprus (physical office or shared workspace)

- Board meetings held in Cyprus (or with a majority of Cypriot directors)

- Sound accounting, annual accounts and annual audit in Cyprus

- A Cypriot bank account for the holding company

If you move to Cyprus in person, you automatically meet most requirements. The annual compliance costs typically amount to €2,500–4,000, including bookkeeping, auditing, and office address.

Common structures with a Cyprus holding company

Owner with multiple operating companies: Founder owns 100% of the Cyprus holding company; the holding company owns operating companies in various jurisdictions. Profits flow upwards as exempt dividends; the founder receives personal dividends as a Non-Domain at 0%.

Parent-subsidiary structure (BE/NL + Cyprus): Belgian or Dutch operating BV pays dividends to a Cyprus holding company via the EU Parent-Subsidiary Directive, 0% withholding tax. The holding company accumulates capital tax-free. The founder distributes the funds privately at their own pace.

IP + operational separation: Cyprus holding company owns the IP and a foreign entity runs the business. Operating company pays royalties to Cyprus (2.5% effective rate); remaining profit distributed as dividend to Non-Dom founder (0%).

Pre-exit restructuring: The entrepreneur immediately owns an operating company. Prior to a planned exit, a Cyprus holding company is inserted via a tax-neutral reorganization. The operating company is subsequently sold via the holding company: 0% CGT.

How do you set up a Cyprus holding company?

Cyprus company formation is fast and simple. From order to incorporation: 5–10 working days. The key steps:

- Register the company name with the Cypriot Commercial Register

- Draft the Memorandum and Articles of Association: constitutional documents that establish the purpose, share structure, and governance.

- Appoint directors and secretary: at least one Cyprus resident director for substance

- Register with the Trade Register and obtain a registration number.

- Register with the Cypriot Tax and Customs Administration and obtain a TIN.

- Open a Cypriot bank account: allow 2–6 weeks for KYC/AML procedures

- Appoint a certified public accountant: annual IFRS-compliant audit mandatory

Total formation cost: approximately €1,650 – 2,500. Annual operating costs: €2,500 – 4,000.

Do you want this fully outsourced and operational, including bank account and compliance? Check out the done-for-you service from Cyprus-Consult →

Compliance: Cyprus is not offshore

Cyprus is fully integrated into international tax transparency frameworks. This is not a grey offshore jurisdiction; it is a fully compliant EU Member State

- OECD BEPS: fully implemented

- Common Reporting Standard (CRS): automatic information exchange

- EU Anti-Money Laundering Directives: full compliance

- Automatic Exchange of Information (AEOI): active participation

- Annual audit required: IFRS-compliant financial statements by a certified public accountant

The Cyprus holding company structure is a legitimate, OECD-compliant use of a truly competitive tax jurisdiction within the EU. Properly set up, it withstands scrutiny by any EU or OECD tax authority.

Ready to set up a Cyprus holding company?

Cyprus-Consult helps founders, entrepreneurs, and investors with structuring, establishing, and maintaining Cyprus holding companies, from initial planning and jurisdiction analysis to company formation, banking, and ongoing compliance.

Do you want to know what a Cyprus holding structure means for your specific situation, tax savings, required steps, timeline, and costs?